A lot of home owners are preparing for a significant increase in their home loan repayments, as their one and two year fixed interest rate terms come to an end. Everyone’s situation is different, but it’s fair to say that the extra interest cost will be challenging for most home owners.

If you’re worried about how you’ll cope, you might find it helps to talk with a financial adviser. There’s nothing like having an experienced expert on your side. In the meantime, here are some helpful points to consider.

How to calculate the extra required

If your interest rate increases from something like 4.0% to 6.5%, that’s obviously a 2.5% increase. But how do you translate that into the extra you’ll have to pay each time? A good way is to use a home loan repayments calculator, like the one on mortgages.co.nz.

To get an indication of your new minimum repayments:

- For the loan amount, enter the amount you still owe

- For the loan term, enter remaining years of your original loan term

- Manually enter the new interest rate

- Choose your current repayment frequency – monthly, fortnightly or weekly

You can now compare the result with your current repayment to see the difference.

Example

When an $800,000 home loan balance with 25 years remaining on its term changes from 4.0% to 6.5% the fortnightly repayment will increase by $544.

Tips

If you’ve been paying more than the minimum required – to repay your loan faster while interest rates were low – the new minimum repayments might not be much more than you’re paying now. However, your loan won’t be fully repaid until the original end date, so you’ll pay interest for longer.

If you’d like to keep your shortened term in your calculations, just enter the time remaining until that nearer end date in step two above.

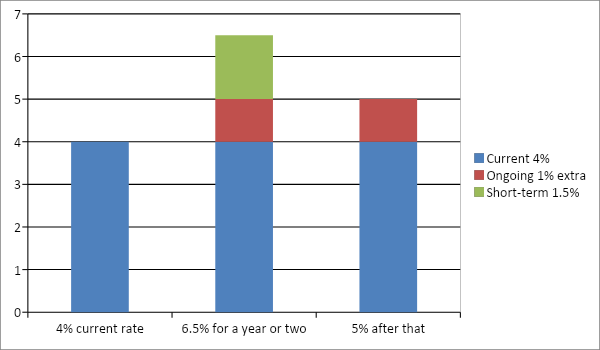

Some of the increase is likely to be short term

While nobody can accurately see into the future, some commentators think the one-year fixed rate will fall back to around 5% in a year’s time, or possibly two years, and then stabilise. That would look like this.

If this prediction turns out to be correct, it means you may only need to budget for a 5% rate over the long term, which in the above example works out at an extra 1% or $210 a fortnight.

However, for the first year or two you would need that ongoing 1% increase, plus an extra 1.5% a year to cover the full initial increase from 4% to 6.5%. Using the above calculator for a $800,000 loan with a remaining term of 25 years, the difference in repayments between 5% and 6.5% interest is $334 a fortnight or $8,684 over a year.

This view allows you to take a two-pronged approach:

- You can immediately adjust your budget to permanently cover the longer lasting increase in home loan repayments – 4% to 5% or $210 extra a fortnight in the above example

- You can also focus on how to finance the additional short-term amount for a year or two – 5% to 6.5% or another $334 extra a fortnight in the above example, which is $8,684 over a year

Let’s start with some ideas for the short-term extra, which is over and above the immediate ongoing increase.

Changing your home loan provider to get a cashback

At the time of writing, the main banks are offering substantial one-off cash payments to new home loan customers who have at least 20% equity in their home. These ‘limited-time-only’ offers tend to be around 1% of the amount you’re borrowing.

For the $800,000 home loan balance above, it works out at $8,000 cash. This would go a long way towards covering the short-term 1.5% extra required until interest rates settle back to around 5%.

However, there are some potential downsides to consider.

- Most cashback offers involve staying with the new provider for up to four years. This could limit your ability to switch for better rates during that time.

- If you received a cashback when you took out your current home loan, switching would probably mean you have to repay some or all of it, depending on how long ago you received it.

- There are costs involved in switching, such as lawyer fees of about $1,000 and probably having to get a new registered valuation for the property. However, some lenders will contribute to these costs or cover them fully.

The free information website, mortgages.co.nz, has a helpful section on refinancing your mortgage.

Changing your home loan provider to get a lower interest rate

It’s always a good idea to shop around whenever your fixed interest rate is coming to an end. This is when you can switch without paying fixed interest rate early repayment penalties. However, as mentioned above, there may be some costs involved in changing lenders.

One of the easiest ways to shop around is to talk to an expert mortgage broker (adviser) who represents most of the main home loan providers. They know who’s offering the best rates and can often access special deals. A mortgage adviser is paid by the lender you decide to go with, so there’s normally no charge for their services. Mortgages.co.nz offers a free find a mortgage broker service.

Restructure your home loan for a better set up

You can do this with your current lender or when switching to a new one. A different home loan structure might reduce your regular repayments.

One example is changing your loan to a longer term. While this means it will take longer to become mortgage-free and you’ll pay more interest over the life of your loan, it might help for a year or two – until you can afford to shorten it again.

Another example is putting some of your borrowing into an offsetting home loan. Although these have a floating interest rate, which is higher than fixed, they allow money in a linked bank account to reduce the loan balance when it comes to calculating interest. The trick is to pay your wages or salary into the offsetting account and have a loan that’s about the same amount, so it’s fully offset and attracts no interest. You then pay for your everyday purchases with a credit card, keeping the loan fully offset until you repay your credit card in full and your next salary payment comes in.

Cut down to one car for a year or so

If you own your home with someone else and you both have a car, maybe you could manage with one car for a while. It might provide the extra money you need to get through the short-term high interest rate period. Plus you’d save on running costs, which can be around $6,000 a year (not including the amount your car loses in value every 12 months). Sure, you might have some occasional ride share and regular public transport costs, but you could be surprised at how much you save overall.

De-clutter for cash

Many people have quite a lot of unnecessary stuff that other people would be happy to buy. With the current high cost of living, more and more people are buying what they need on Trade Me, rather than shopping for new.

Take a good look at your wardrobe, storage areas and spare room. If you find things you haven’t used in a year, maybe you could manage without them. Selling on Trade Me is really easy.

While you’re at it, you could even set yourself a planet-friendly goal like not buying any new clothes for a year. If you really need something, find a recycle boutique.

Take in a boarder/flatmate for a year

Got a spare room that’s mainly used for storage? Maybe you could clear it out and make some money by renting it out. Check out the ‘flatmates wanted’ section of Trade Me to get an idea of what you might be able to charge for a similar room in your area.

The rent will be taxable income for you, but if it includes some expenses – like a share of the utilities – these may be tax deductible. It also pays to talk with your insurance company to see if your home and contents policy would be affected.

If you decide to go ahead, it’s a good idea to write up an agreement covering when rent is due, what happens about food and utilities, whether chores are to be shared and what you expect regarding noise, visitors and parking.

Earn a side-gig income

If you have unused skills and experience, or quite a bit of spare time, you may be able to generate extra income. Lots of work can be done on a casual basis from home these days. Also, many employers are looking for people who can come in for a few hours to cover their peak periods. Once peak interest rates have passed, you have the option of turning your side gig off or keeping it going to accelerate your journey to being mortgage free.

How to cover the long-term increase in your home loan repayments

It’s very unlikely that home loan interest rates will return to the record lows of recent years, so a permanent change to something like the 5% mentioned above is likely. The only way to cover this is to budget for it. That might mean adjusting your income and/or expenses, so you can avoid the stress of constantly worrying about your home loan repayments.

If you’re struggling to make this work, there are free budgeting services that could help or you could talk to a mortgage adviser. They might help you find a way to pay less interest than your current lender is about to charge.

If you ever think you’re about to miss an upcoming home loan repayment, it’s important to talk with your lender as soon as possible. They may be able to help with immediate short-term options, such as a brief repayment holiday or an interest-only period while you find a more permanent solution.

For financial tips and help with budgeting, visit the free government-funded website sorted.org.nz.